FA Back 3.28 - Release notes

Released: September 2025 as a part of Q3 2025 release

FA Back 3.28 introduces a number of new features and improvements in rebancing, bond features, contact properties, asset transfer's ex-post costs and corporate actions.

Conservative sell logic for rebalancing

Why?

Previously, when producing sell orders, rebalancing took into account current positions and any positions that are expected from existing orders. In some cases, this approach created an operational risk, especially when existing amount-based buy orders (common for fund positions) were involved. The market price changes affect the number of units you receive, thus making it risky to take a buy order into account.

Who is this for?

This feature is for portfolio managers and operations teams who rebalance portfolios and want to avoid short positions for regulatory or operational reasons.

Details

A new option for conservative rebalancing applies stricter rules to sells. You can now choose if sell suggestions are based only on current holdings minus sell orders or on current holdings, including all existing buys and sells. In the Rebalance window, the Sell from field lets you select:

Positions minus sell orders – Ensures that suggested sells are based strictly on what the portfolio currently holds. This option prevents you from short positions, especially in case you have existing trade-amount-based buy orders, and the target requires creating unit-based sells, and the market prices have increased after buying (see the example below).

Positions minus sell orders plus buy orders – Matches the behavior of previous versions. This is the default option – if you prefer the original workflow, no changes are needed.

Example: The portfolio holds 100 units of Security A at 10€ (value 1,000€). There is an existing sell order for 100 units (from a model change) and an existing trade-amount-based buy order of 100€. With Positions minus sell orders plus buy orders, rebalancing includes the expected buy, and suggests selling 110 units in total. However, when the buy order settles at a new price of 11€, it delivers only 9 units instead of the estimated 10. This leaves the portfolio with 109 units against 110 sold, resulting in a short position of 1 unit. With "Positions minus sell orders", the system only sells current portfolio holdings, and you can repeat rebalancing after the buys settle.

Learn more: Rebalance window.

Bonds

In Q3 2025, we continue to expand support for fixed income instruments and adapt to different market conventions. This release includes updates for discount-rate instruments, fixing generation for floating-rate notes, separate day count conventions, trade increment validation, and redemption yield periodicity.

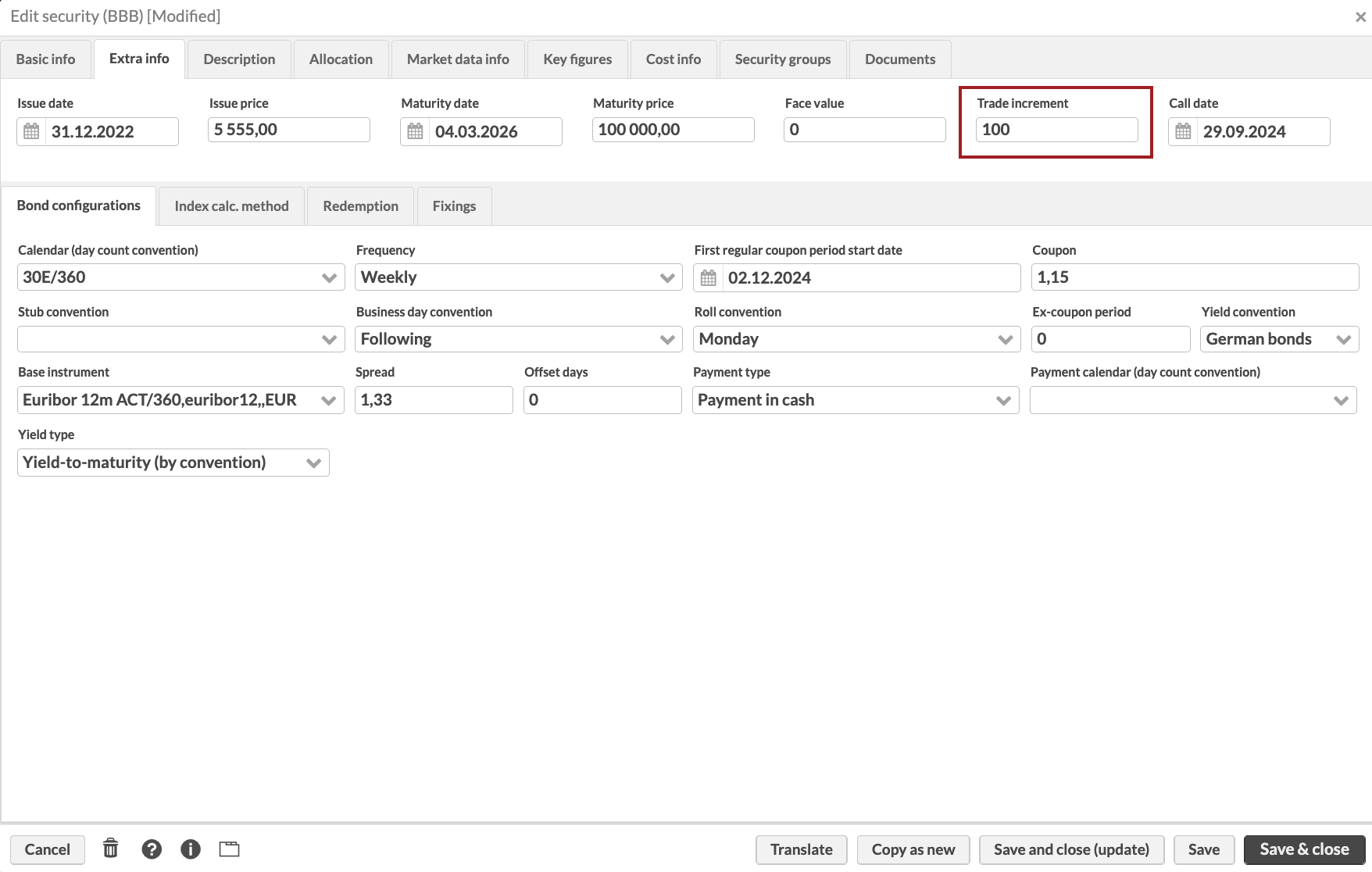

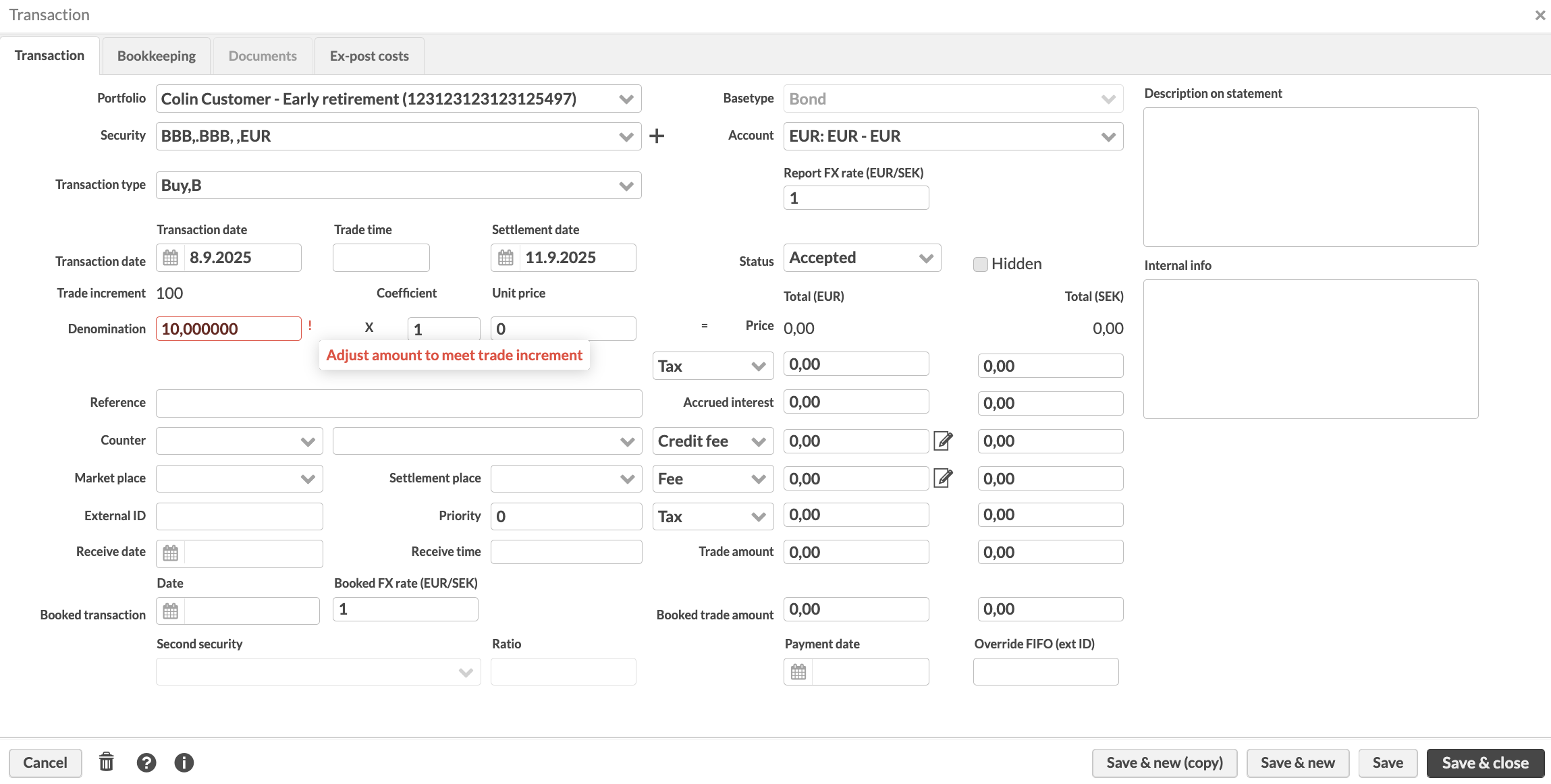

Trade increment for bonds

Why?

Some bonds have a trade increment that defines the smallest amount by which a bond can be traded (for example, 500 or 1000 units). Previously, FA system allowed creating trades that don’t meet this requirement, which could lead to trade orders being rejected at a later stage. Now, the system validates the denomination when creating an order or transaction. This way, you don’t have to cross-check the trades with security properties, and can be sure that the orders meet the trade increment requirement.

Who is this for?

This feature is for portfolio managers working with fixed-income securities.

Details

A new Trade increment field was added to the Security window under the Extra info tab. This field defines the minimum amount by which a bond can be traded. When you enter trades, you can see the bond’s trade increment in the Transaction or Trade order window, and the Denomination value is validated to match the trade increment.

|

|

Learn more: Security window, Securities and market prices import.

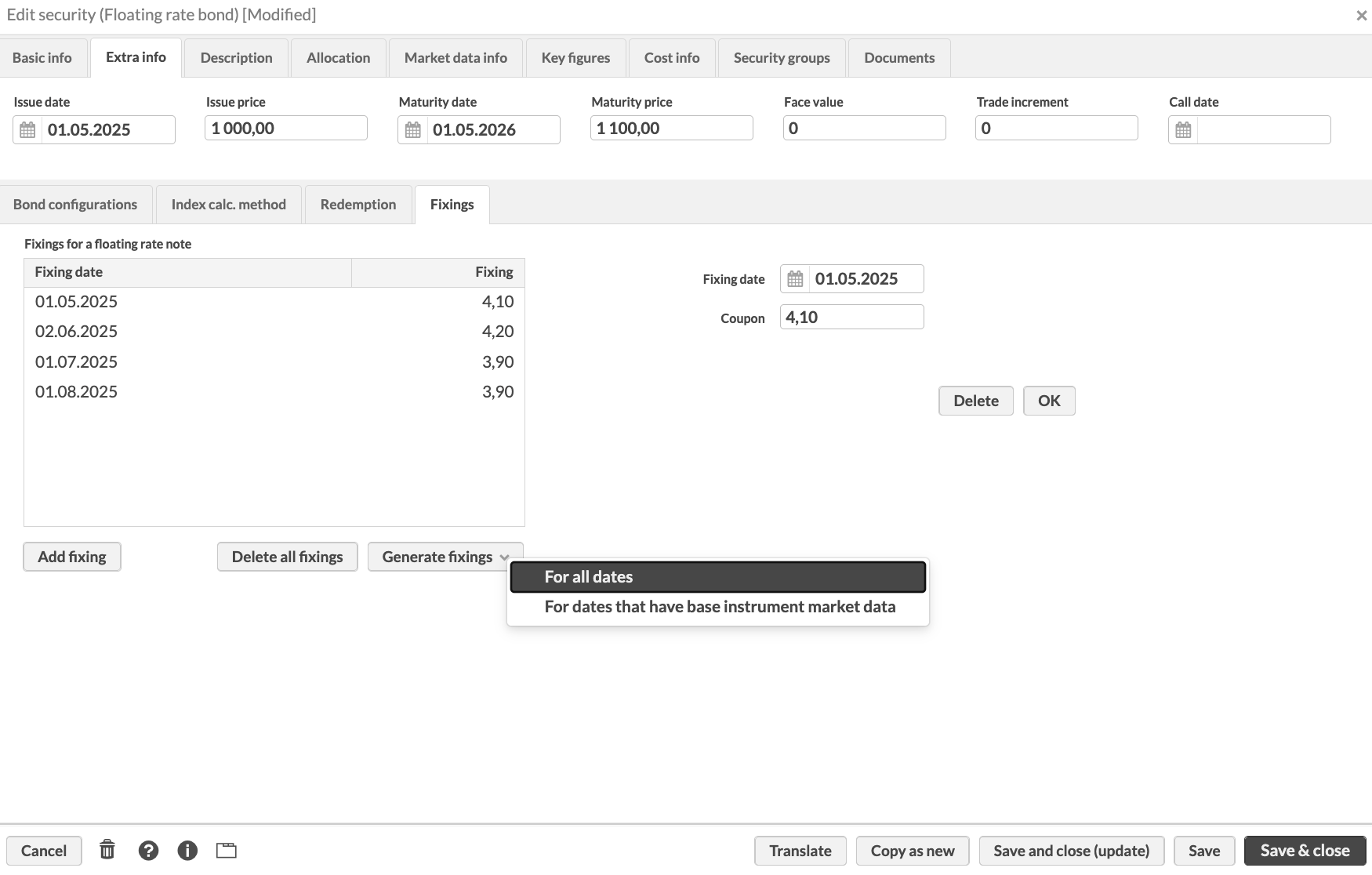

Improved fixing generation for floating rate bonds

Why?

Previously, when generating coupon dates and rates for a floating rate bond in the Security window, the system ignored the bond’s base instrument and spread. This always resulted in fixings with a zero value, even if valid market data existed. While it was possible to generate correct fixings using the bulk Securities view → Update security data → Generate fixings process, users could not view or generate accurate fixings directly in the Security window while working with a bond.

Who is this for?

This improvement is for operations teams who manage floating-rate notes (FRNs).

Details

The Generate fixings button in the Security window → Extra info → Fixings tab now calculates historical coupon rates using the base instrument market data and the spread. In addition, you can now choose to generate rates:

For all dates – Add one row for every coupon date. If base instrument market data is missing on the fixing date (after applying the offset days), the system falls back to the Coupon value from the Bond configurations tab.

For dates that have base instrument market data – Adds rows only when base instrument market data is available on the fixing date (after applying the offset days).

Note that generating coupon information for fixed rate bonds in the Fixing tab works as before. Also, mass-generation of fixings via the Update security data → Generate fixings in the Securities view did not change.

|

Learn more: Security window, Fixed and floating rate bonds

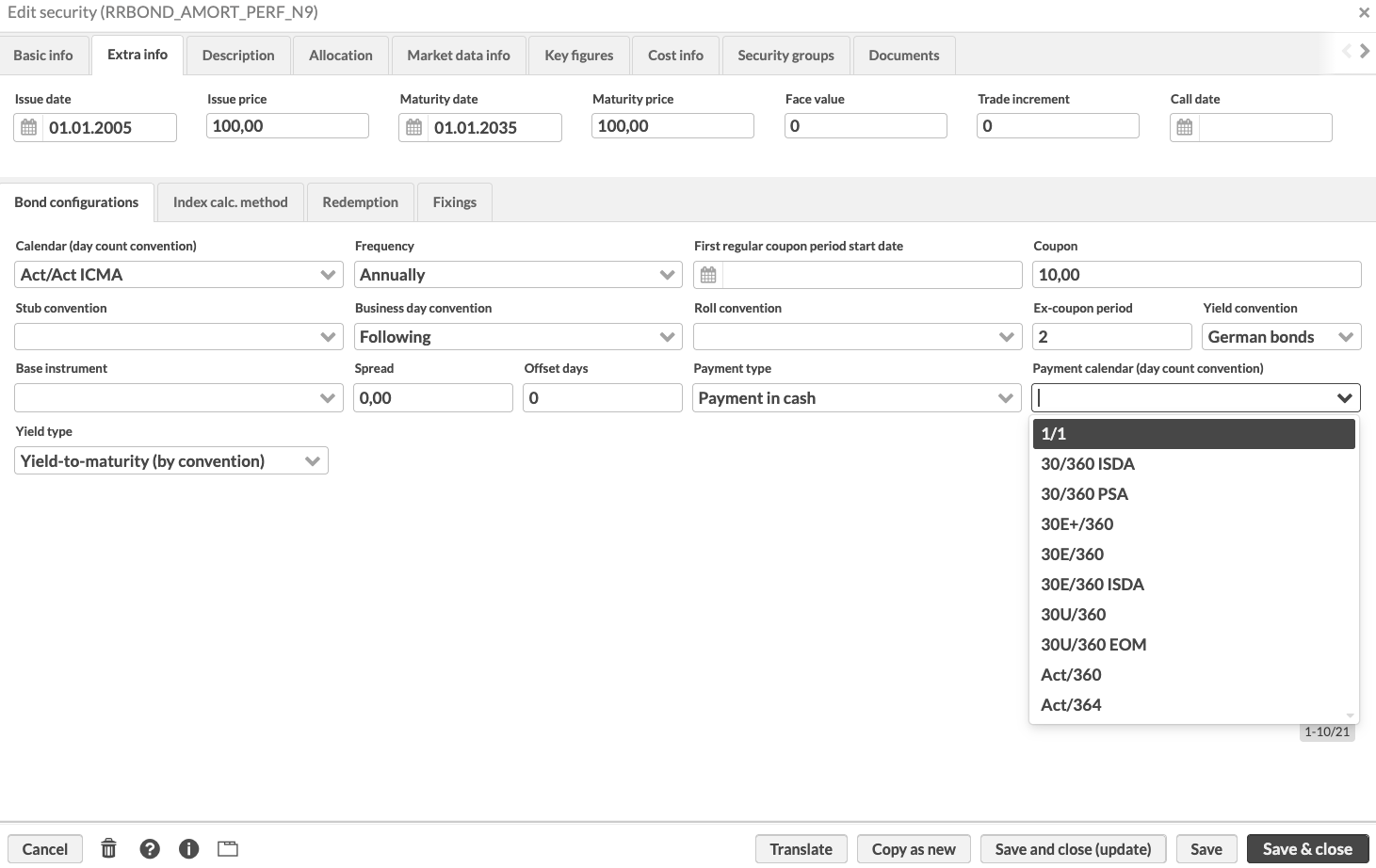

Separate day count conventions for accrued interest and coupon payments

Why?

In some markets, such as Norway, fixed rate bonds follow different day count conventions for different purposes. Accrued interest for transactions and portfolio valuation is calculated using one convention (for example, Act/365), while coupon interest is calculated using another convention (for example, 30E/360). Previously, FA supported only a single day count convention per security, used both for calculating accrued interest and coupon payments.The new feature allows you to define separate day count conventions for accrued interest and coupon payments, ensuring both are calculated correctly.

Who is this for?

This feature is designed for portfolio managers and operations teams handling bonds where accrued interest and coupon payments follow different conventions.

Details

New Payment calendar (day count convention) in Security window, Extra info tab lets you lets you set a separate convention for coupon calculations. The field is optional. If left empty, the convention from Calendar (day count convention) is used for both accrued interest and coupon payments.

|

Learn more: Security window, Securities and market prices import.

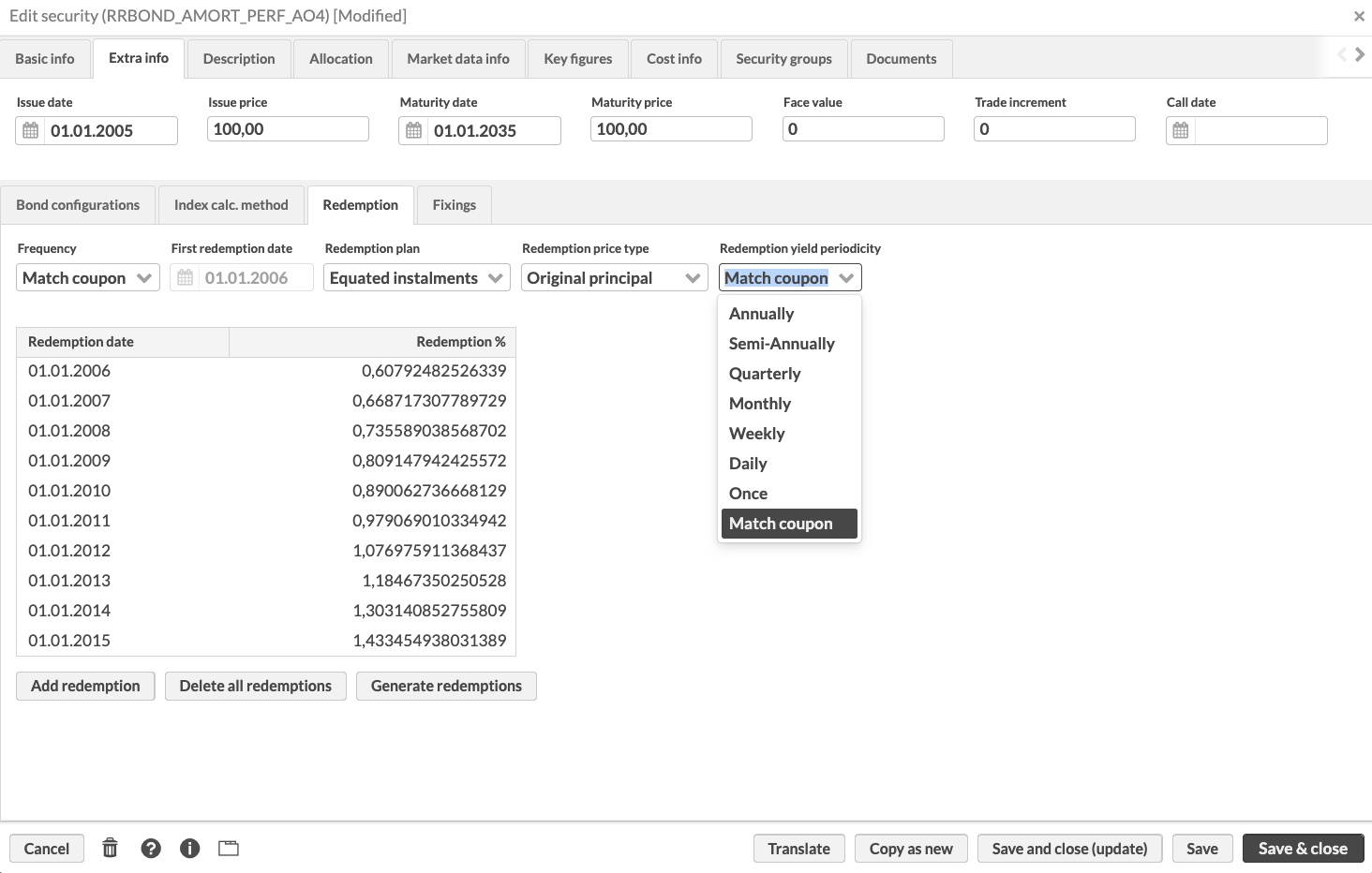

Redemption yield periodicity

Why?

Previously, FA system calculated the redemption yield for bonds using the coupon frequency as the compounding assumption. This default approach always presented the yield as annualized, following the German/True convention, which is the most common practice in European domestic markets. With this enhancement, FA system now also supports other market conventions, such as the UK and US, where semi-annual compounding is standard.

Who is this for?

This feature is for operations teams who work with fixed income securities. It is particularly useful when dealing with amortizing bonds.

Details

You can now specify the Redemption yield periodicity in the Security window, Extra info, Redemption tab. This setting defines how often the yield is compounded for calculation and presentation in Analytics+.

Options include:

Annually, Semi-annually, Quarterly, Monthly, Weekly, Daily.

Match coupon (default) – Use the coupon frequency defined in the Bond configurations tab.

Changing the periodicity affects yield-to-maturity calculations but does not change the bond’s actual cashflows.

|

Learn more:Security window, Securities and market prices import.

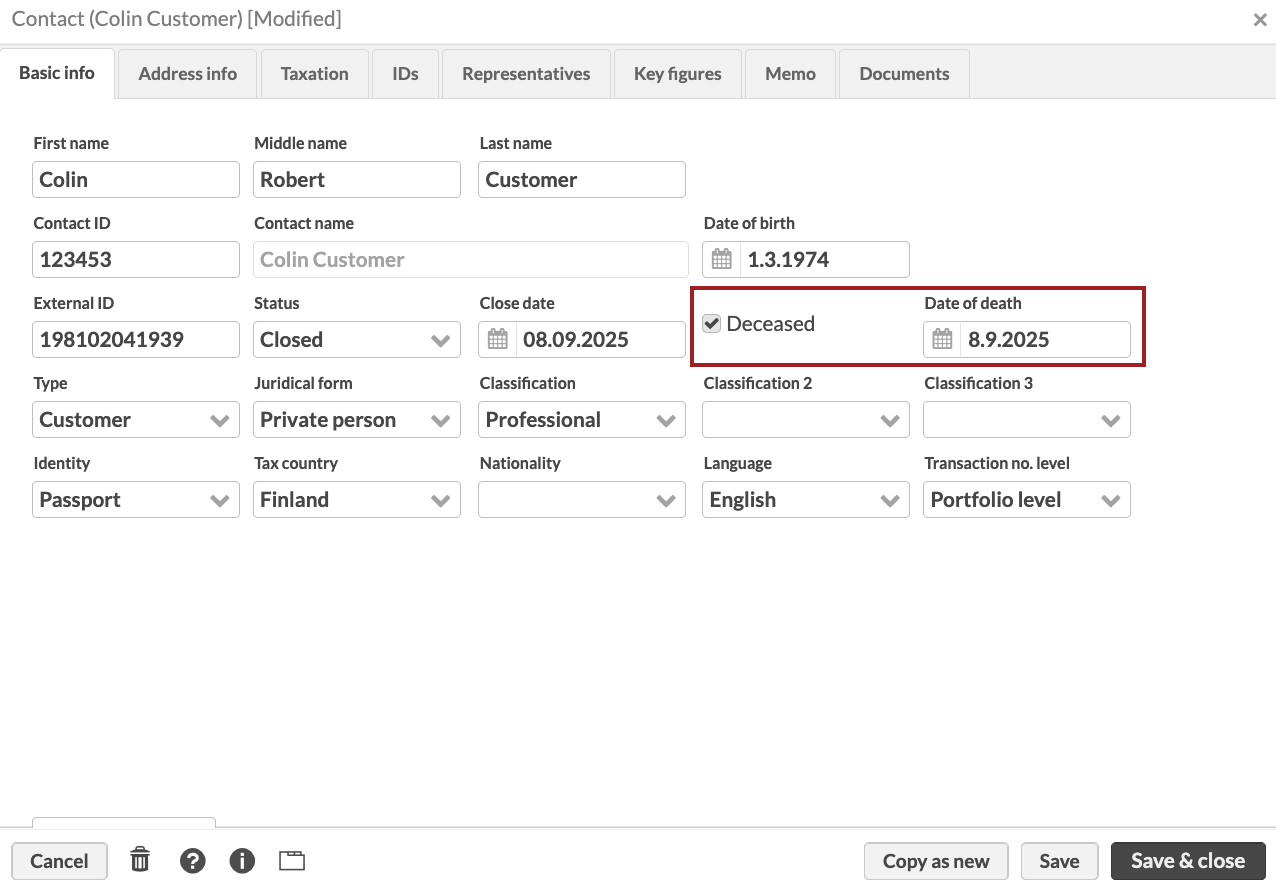

Marking a contact as deceased

Why?

We added new fields that allow you to mark a contact as deceased and add the date of the person’s death. This is useful for maintaining accurate customer information and avoid uncomfortable situations when communicating with clients or their family members.

Who is this for?

This feature is for users who set up and maintain client information, as well as for any users who are in contact with clients.

Details

You can find the new Deceased and Date of death fields in the Contact window, Basic info tab. While these fields don't trigger automated actions, they can be used for filtering, reporting, and keeping records up to date.

|

Learn more: Contact window, Contacts import.

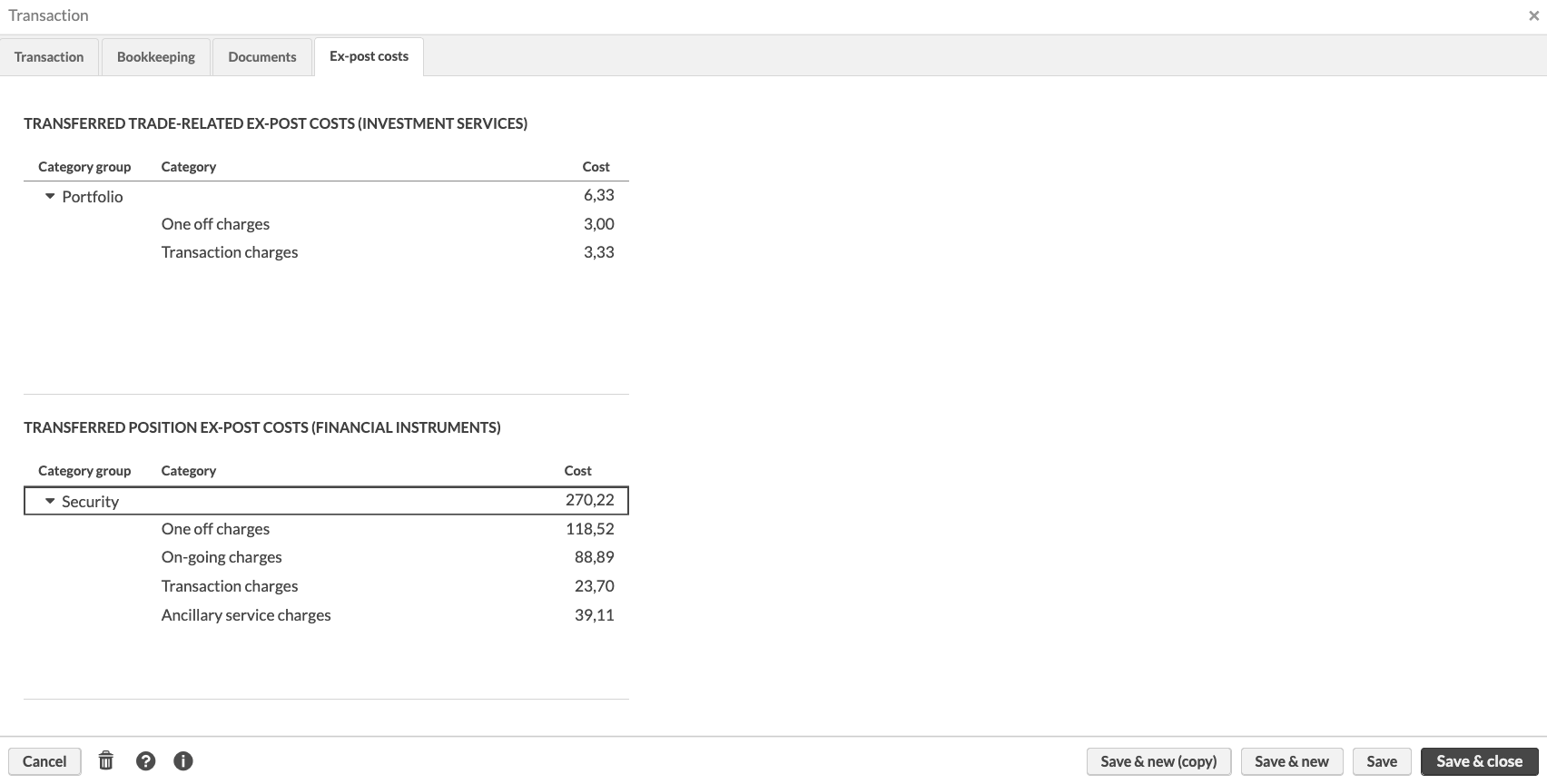

Ex-post costs related to transferred positions

Why?

When positions are moved between portfolios – such as during pledging or asset transfers – accumulated ex-post costs are transferred with the position. These costs can significantly impact portfolio performance analysis, cost transparency, and reporting. Before, transferred ex-post costs weren’t visible – now, you can view them in the related transactions.

Who is this for?

This improvement is for users who need to see ex-post cost breakdowns for costs transferred when moving positions.

Details

We added a new tab called Ex-post costs to the Transaction and Trade order windows. The new tab shows costs related to the transferred position:

Trade-related ex-post costs – ESMA-classified breakdown of costs associated with the transaction or trade order.

Transferred position ex-post costs – Accumulated ex-post costs moved with the position.

|

Learn more: Transaction window, Pledge portfolios, positions and purchase lots, Transfer assets between portfolios.

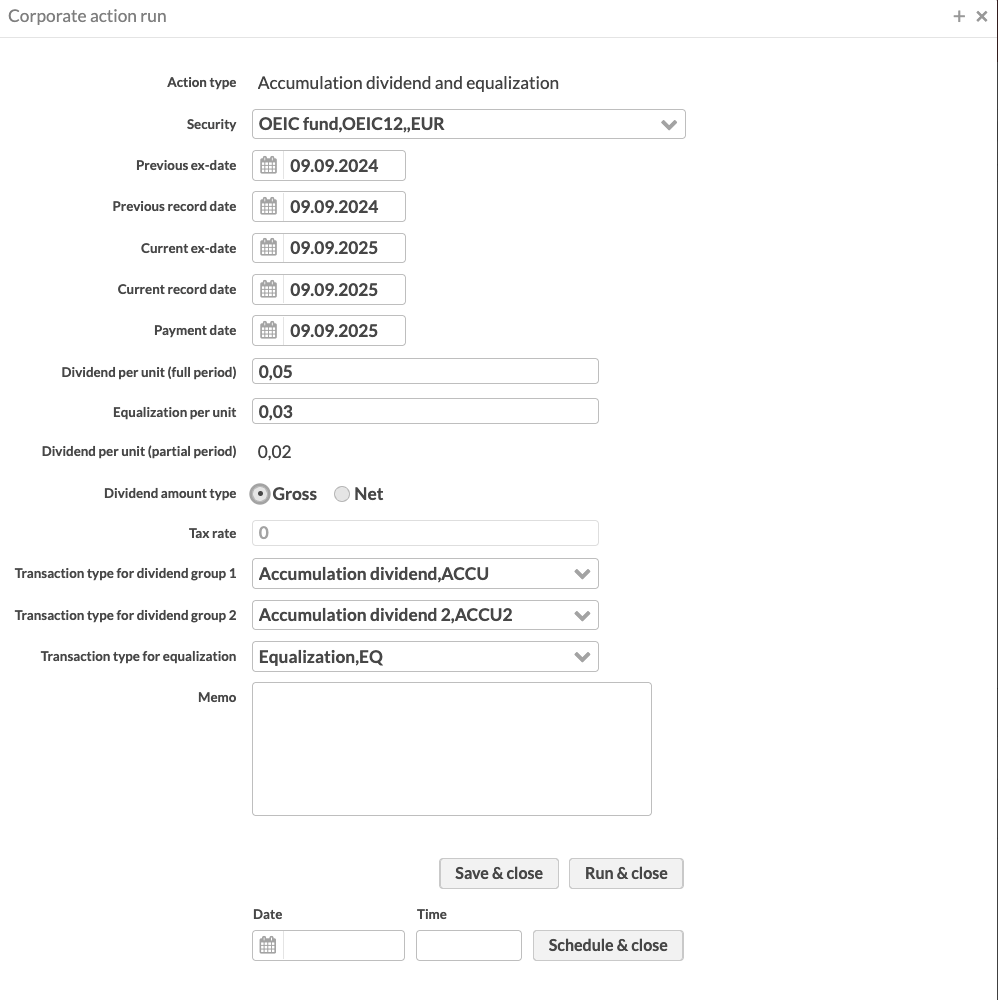

Accumulation dividend and equalization

Why?

Open-ended investment companies (OEICs) operating in the UK market reinvest the income they earn, which increases the fund’s unit price. To support this, we introduced the Accumulation dividend and equalization corporate action to record reinvested income for tax purposes and reflect equalization in customers’ portfolios.

Who is this for?

This feature is for operations teams who record and execute corporate actions.

Details

The Accumulation dividends with equalization corporate action applies to all shareholders who own fund units. Instead of being paid out as cash, the dividend is reflected in the fund’s unit price. Unit holdings are divided into two groups, with different transactions generated by the FA system:

Group 1 – Full-period holdings (owned before the previous ex-date and kept until the current ex-date): The system generates accumulation dividend transactions for tax reporting.

Group 2 – Partial-period holdings (bought on or after previous ex-date and kept to the current ex-date): The system generates both accumulation dividend transactions (for the relevant portion) and equalization transactions that adjust the purchase price in the portfolio.

Accumulation dividend transactions are recorded in portfolios to help investors and accountants report taxable income, even though no cash is received. These dividends are treated as notional income for tax purposes.

Equalization transactions reduce the purchase price of the units, ensuring new investors do not unfairly benefit from income they did not earn.

|

Learn more: Accumulation dividend and equalization, Corporate actions import.

Other improvements

Transactions

We added a new amount effect for transaction type configuration. The effect is called “Reduces amount but not principal” and should be used, for example, to configure paydown transactions for amortizing bonds. Learn more: Preference - Transactions.

Now, limits and limit groups for a portfolio can be imported in the same portfolio import file. Learn more: Portfolios import.

Taxation

The Taxation tab in the Contact window now features CGT profile field. CGT profile is fetched from FA Operations. Learn more: Contact window.

Trade order management

Internal info field for trade orders now includes ExecID from the FIX message. This is the unique ID of an execution message – extracting this ID gives access to the message, which can be used, for example, to build a custom report.

Improved the trade order flow for partially filled orders that expired. Before, the entire order received “Expired” status in FA Back, even though it was partially filled. Now, the order is split in two orders, with “Executed” and “Expired” statuses. The improvement works for all trading platform integrations that use FIX formats.

Fixes

Analytics

Fixed an issue where multiple analytics figures were calculated incorrectly after allocation changes.

Resolved an issue where Analytics+ capped negative returns at -100%. Extremely large negative returns (e.g., -1,000,000%) now display their actual values instead of being limited to -100%.

APIs

Improved access control in GraphQL APIs.

Corporate actions

Made minor text adjustments in the Exchange corporate action window.

The amount row in the corporate action's transaction table is now dynamic and reflects the selected transactions.

Fixed an issue with tags used for defining the default tax rate in a corporate action. Before, some tags that include numbers (for example “Tag1”) didn’t work correctly. Now, these tags are distinguished by the system correctly.

FX contracts

Fixed an issue where FX contract updates could fail due to rules triggering rule re-runs on transactions.

Updates to FA Back 3.28

FA Back 3.28.1 - Release notes

FA Back 3.28.1 is an update to FA Back 3.28. This update includes the following fixes:

Fixed an issue where bond interest was calculated incorrectly after the latest upgrade because the system reset interest twice, causing negative accrued interest.

Fixed an issue where the limit definition import API set some values in wrong fields. Now, "Code for numerator group, sector or tag" field in the numerator and "Filter group by", "Code for group, sector or tag" in denominator are populated correctly.

Fixed an issue where redemption yield for straight line amortizing bonds was too high due to overstated cashflows.

Fixed some issues in Accumulation dividend and equalization corporate action:

Improved the performance for running Accumulation dividend and equalization for a larger number of portfolios.

Fixed the Dividend total in Transaction tab. Now it doesn't include the equalization amount.

Fixed equalization transactions – now they don't include any taxes when generated.

Fixed an issue in the Transactions tab of an already run Accumulation dividend and equalization. The totals row at the bottom now shows correct figures.

Disabled the possibility to re-run Accumulation dividend and equalization. The action is always run for all shareholders at once – there should be no need to re-run it. You can re-run it after deleting an existing run.

Fixed an issue in the Summary tab of an already run Accumulation dividend and equalization. Now it shows the entered “From custody” values and "Difference" values correctly.

Fixed an issue where empty transactions were created if a shareholder didn't have units in both group 1 and group 2.

FA Back 3.28.2 - Release notes

FA Back 3.28.2 is an update to FA Back 3.28. This update includes the following fixes:

The limit definition importer now allows the use of "***" in mandatory fields when updating existing limit definitions, aligning with documentation and improving update flexibility. Mandatory fields are now only enforced when importing new limit definitions.

Fixed an issue that resulted in an error message when selecting “new run” for an Accumulation dividend and equalization that was saved but not yet run.

Fixed several issues related to the summary of the Accumulation dividend and equalization:

After the Accumulation dividend and equalization run, the read-only Excel file now also shows the custody and difference values entered.

The difference calculation on the Accumulation dividend and equalization summary tab now rounds the values according to the security type rounding settings.

Equalization difference had a calculation error and is now calculated correctly.

Resolved an issue in the security importer where the Set settlement period option could be unintentionally disabled during imports. Now, existing values for settlement period settings remain unchanged unless explicitly changed.

Fixed an issue in report scheduling when tags weren't correctly added to the reports.

Fixed an issue where scheduled report generation against empty transaction or trade order views could trigger an error, causing the schedule to be deleted. Now schedule doesn't get deleted and user can see in logs that no items where found.

Redemption periodicity is now considered when calculating price from yield for fixed income securities.