Preference - Portfolios

Portfolio preferences include relevant preferences for managing portfolios. These preferences allow you to set the options available in the fields when defining the basic information in the Portfolio window. The options you set up in these preferences allow you to flexibly group your portfolios. In addition, rebalancing preferences allow you to set up preferences for rebalancing.

Accounts

Define how the system calculates and capitalizes account interest.

- Calculate account interest based on

An option to calculate accrued account interest based on previous or current day's account balance.

Previous day's balance – Calculate accrued interest overnight based on the end-of-day balance.

Current day's balance – Calculate interest so it reflects the current day's balance when the calculation is done.

You can override this selection on the account level in the Portfolio window's Accounts tab.

- Capitalize earned and charged interest with

An option to track and capitalize earned and charged interest in one transaction or separately, using different transaction types.

Same transaction type – Capitalize earned and charged accrued interest at the same time, in one transaction. Choose the transaction type in Transaction type for capitalization.

Different transaction types – Capitalize earned and charged accrued interest separately, using different transaction types. This option is useful if you need to capitalize interest on an overdraft monthly or shortly after it accrues, and pay out interest on positive balance yearly. Different transaction types let you separate earned and charged interest in reports and accounting. Choose transaction types in the Transaction type for earned interest and Transaction type for charged interest fields.

You can override this selection on the account level in the Portfolio window's Accounts tab and also when booking account interest payment.

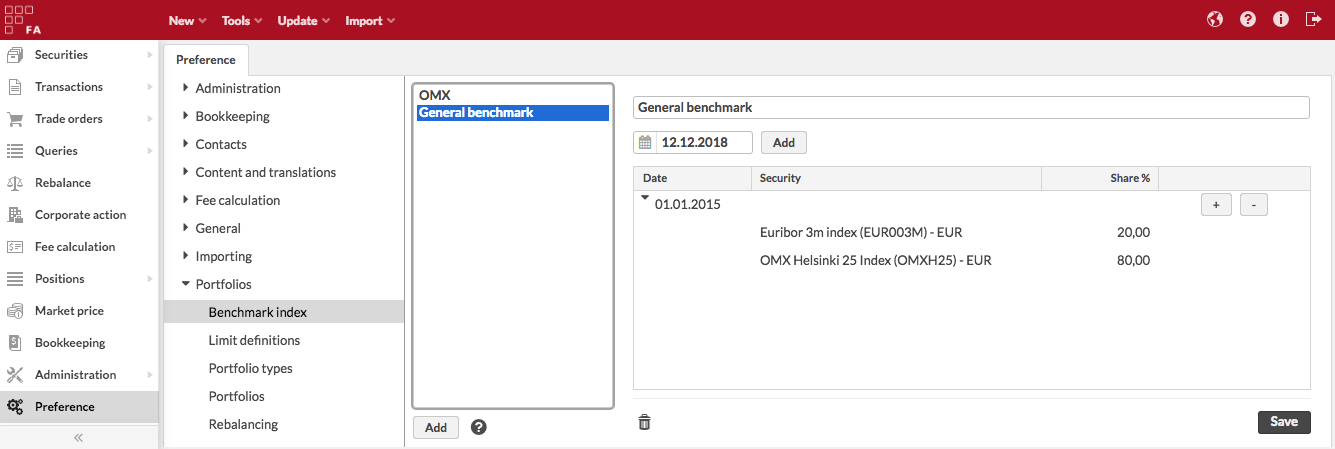

Benchmark index

Benchmark indices are used to compare the performance or return of a portfolio to an index. The benchmark index linked to a portfolio is visible, for example, in some P/L reports, and in Analytics Plus. Benchmark indices can be:

Single or composite. Single benchmarks consist of one index. Composite benchmarks consist of a combination of different indices (for example, a composite of 40 % index A and 60 % index B).

Regular or interpolated. Regular benchmarks are based on the dates and position shares that you entered. For example, you can set a benchmark that is valid from 01.01.2022 and contains 20% of a certain stock. Then, you can raise the position share, for example, to 22% starting from 01.03.2023, and so on. Interpolated benchmarks are based on the position shares on the start and end date of the period. The values between the dates are calculated by the system to create a gradual change that occurs on business days. For example, if you want to reduce investments in a particular sector from 30% to 20% over 5 years, you can enter two dates and specify the start and end position shares. The values in between the dates will be calculated automatically.

General or portfolio-specific. General benchmark indices are defined in Preference. You can then apply them to a portfolio by choosing a general benchmark in the Portfolio window, Benchmark tab. Portfolio-specific benchmarks are defined per portfolio in the Portfolio window.

If multiple portfolios follow the same benchmark index, it is worth defining a general benchmark index. Also, any modifications made to the general benchmark index affect the portfolios linked to the index.

|

Benchmark parameters

The benchmark index information is defined in the fields on the right side of the window (fields marked with * are required):

- Benchmark index name*

The name of the benchmark index.

- Linked portfolio

Source portfolio to copy the benchmark information from. The field is currently not supported. To link a benchmark to a portfolio, use the Portfolio window, Benchmark tab (see Portfolio window in FA Back reference).

- Date

The date from which the benchmark index is valid in a portfolio. This is usually the start date of your portfolio (when the portfolio starts getting in transactions). If you have a regular benchmark, define one date and enter the position shares. You can later update the benchmark by adding a new date and re-defining the index positions. The updated index is valid from the new date onward. If you have an interpolated benchmark, you need to enter at least two dates: the start and end date of the change. For example, if you set a start date to 8.10.2022, the position shares get changed on 9.10.2022.

- Interpolate shares between dates

Whether a benchmark is interpolated.

- Holiday calendar

For an interpolated benchmark, set the holiday calendar to use. Position shares change only on business days.

Benchmark content

Under each date in the table, you can see the index content. To add a position, click Add in the table row.

- Date

See the Date field description above.

- Security

The security the index follows. If you add securities in other currency than the portfolio's currency, the index values are converted to your portfolio's currency with a relevant FX rate.

For interpolated benchmarks, the start and end date indices must contain the same set of securities. If you want a position to be sold out gradually, add it with 0% weight on the end date.

- Share %

The position share in the index. Position shares of different securities under one date must sum up to 100.

Limit definitions

Limit definition preferences allow you to define limits or investment constraints that you can link to your portfolios for limit monitoring. For more information, see Limit analysis.

Portfolio types

Portfolio types are used to categorize the portfolios: for example, the portfolios could be divided into investment portfolios and insurance portfolios. For a portfolio, portfolio type is mandatory.

A portfolio type consists of a code and a name: the code is used to identify the portfolio type in the system, and the name is used to view and choose the portfolio type in the user interface. You can also mark the portfolio type as CGT applicable.

Portfolio types that come with the Standard solution are listed in the table. If your business flow requires some other types, you can add more. You can also redefine the names for existing portfolio types in Preference → Content and translations → Translations. We don't recommend deleting standard portfolio types or modifying the code, as they will be restored with the next system upgrade.

Code | Name |

|---|---|

FUND | Fund portfolio. |

FXH | FX hedge portfolio |

INS | Insurance portfolio |

INV | Investment portfolio |

Restricting access to portfolio types

Portfolio types also support restricting them to be shown only to specific user roles, allowing you to restrict the list of available portfolio types per user role within the Portfolio type dropdown in the Portfolio window, Basic info tab and Portfolio view's extended search fields. For example, you can decide which user role(s) are allowed to use which portfolio types for the portfolios they manage, especially useful in restricting the visibility of custom fields linked to a certain portfolio type.

If you want to restrict a portfolio type to be shown to only certain user role(s), you can do this by checking the appropriate roles within the Portfolio type preferences - Once checked, the type will be available only to the users with the selected role(s). If you don’t restrict a portfolio type to a specific user role, it will be visible to all users.

To enable CGT calculations for the portfolio type, tick the CGT applicable checkbox.

Portfolios

Portfolio preferences allow you to enable different settings related to portfolios.

- Generate a running number for portfolio ID automatically

When enabled, a running number is automatically created for a new portfolio as the portfolio ID, starting from number 1. When enabled, the next available number is set as the portfolio ID in the Portfolio window.

- Show memos for all of the selected customer's portfolios on the overview

When enabled, the Memo section on the Overview shows the memos for all of the selected customer's portfolios at the same time, instead of showing only the memo of the selected customer or portfolio.

Note

Enabling this might slow down opening customers with lots of portfolios under them on the Overview.

- Define the maximum number of portfolios shown in the "Portfolio hierarchy" tree in Overview

You can configure how many portfolios are shown in the "Portfolio hierarchy" section in Overview, allowing you to control how many portfolios are shown for example when viewing a large portfolio group. By default, 500 portfolios are shown.

Pledging and unpledging

The Transaction types for pledging and unpledging section contains the following settings:

- Removing position from portfolio

Configure the transaction type the system uses to create "remove" transactions in the portfolio from which the position is removed when you pledge or unpledge it.

- Adding position to portfolio

Configure the transaction type the system uses to create "add" transactions in the portfolio to which the position is moved when you pledge or unpledge it.

- Tax type for pledging and unpledging

Define the tax type to record profit-affecting taxes when pledging and unpledging. If the original transaction includes a tax with a cash effect, that tax type is used in pledging and unpledging transactions.

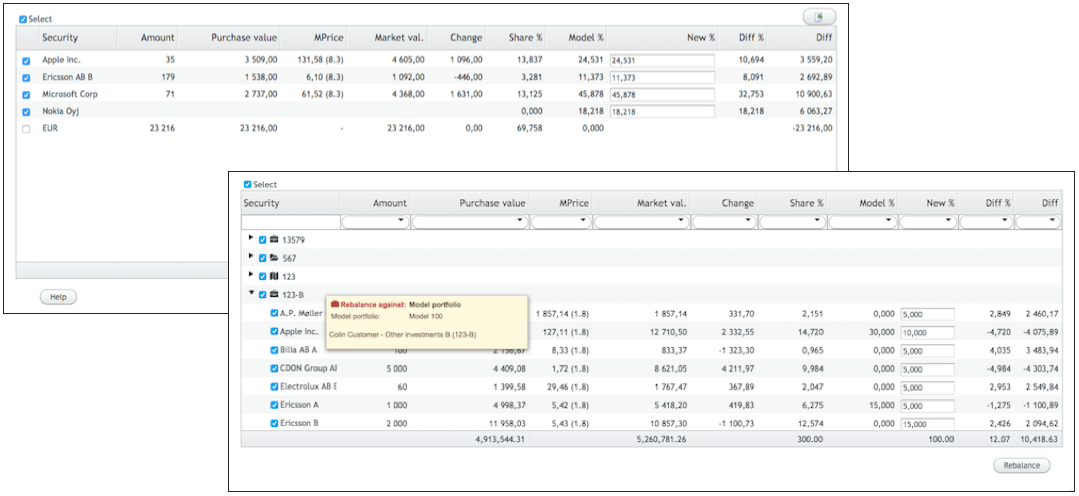

Rebalancing

In the Rebalancing preferences, you can define the method for creating trade orders from rebalancing as well as the transaction types used in creating buy and sell trade orders when rebalancing a portfolio.

First, define the method trade orders are created by rebalancing.

- Create trade orders based on trade amount (calculate unit price based on amount and difference)

Choose this option if you want to fix the amount and trade amount of the trade orders created by rebalancing and adjust the unit price to match the amount * unit price = trade amount (default option). With this option, you will end up with trade orders that should be executed "with trade amount", since the trade amount equals the difference in the position between the rebalanced portfolio and the model portfolio.

However, when selling away an entire position or all securities in the portfolio, the trade orders are always calculated based on the amount/units. In addition, in such a scenario, you can set up rebalancing to create the sell trade orders with a different transaction type (see Select the transaction type used for trade orders when selling an entire position below).

- Create trade orders based on the amount (calculate trade amount based on the amount and market unit price)

Choose this option if you instead want to fix the amount and unit price of the trade orders created by rebalancing and adjust the trade amount to match the amount * unit price = trade amount. With this option, you will end up with trade orders that should be executed "with the amount", since the amount and unit price equal the difference in the position between the rebalanced portfolio and the model portfolio on the rebalancing date.

Despite the method you selected, the trade orders are formed with the same logic, and the amount is always calculated in the same way - this selection determines whether the final trade orders are created by adjusting the unit price or trade amount to achieve valid calculations for amount * unit price = trade amount.

Example: you need to buy for 300 €, your unit price is 8 € per share. → Number of shares you need is 300 € / 8 € = 37,5. However, if you are buying a stock with 0 decimals allowed, then you actually get only 37 shares. Preferences come into play on what to adjust in the order:

The “Create trade orders based on trade amount (calculate unit price based on amount and difference)” option fixes amount (37 shares) and difference (300 €), and then recalculates the unit price based on them: 37 * 8,108108.. € = 300 €

The “Create trade orders based on amount (calculate trade amount based on amount and unit price)” option fixes amount (37 shares) and unit price (8 € ), and then recalculates the trade amount based on them: 37 * 8 € = 296 €

Trade orders created by rebalancing indicate whether the trade order was created based on trade amount or units, as defined in the Rebalancing Preferences. This information is stored on the trade order as trade order's Execution method (available from FA 3.8 onward) and in trade order's "Internal info" as follows:

"Create trade orders based on trade amount" results in trade orders with execution method "Net trade amount" and internal info "type=CASH".

"Create trade orders based on amount" results in trade orders with execution method "Units" and internal info type=UNITS.

When you are using the default setting to "Create trade orders based on trade amount", most trade orders are calculated based on the trade amount (execution method "Net trade amount" and internal info "type=CASH"), but when selling away an entire position or all securities in the portfolio, the trade orders are always calculated based on the amount / units (execution method "Units" and internal info type=UNITS). In addition, in such a scenario, rebalancing supports creating the "sell units" trade orders with a different transaction type (configurable in Rebalancing Preferences).

Below, define the transaction types used for the created trade orders, and when the trade orders are executed, for the transactions recorded to the portfolios.

- Select the transaction type for "buy" trade orders (mandatory)

Choose the transaction type used to create buy trade orders from rebalancing. This is the transaction type used for all buys.

- Select the transaction type for "sell" trade orders (mandatory)

Choose the transaction type used to create sell trade orders from rebalancing. This is the default transaction type used for sells.

- Select the transaction type used for trade orders when selling an entire position (optional, if not defined, then the selected "sell" type is used)

Choose the transaction type used for sell trade orders when rebalancing creates a sell trade order based on units instead of trade amount, for example when selling away an entire position from a portfolio. If left empty, the selected sell type is used for all kinds of sell trade orders.

Below, you can define a target range for the portfolio's cash balance or buffer for cash to ensure a positive cash balance. These preferences specifically affect what kind of trade orders are created when rebalancing is restricted to accounts.

- Define the target range for the portfolio's cash balance (when rebalancing cash, the portfolio is rebalanced only if cash is outside of the target range)

Define a target range, or minimum and maximum, for the portfolio's cash balance: When restricting rebalancing to accounts, the portfolio is rebalanced and trade orders are created only if cash is outside of the defined target range. You can for example define that if there is between $0 and $10 on your account, the portfolio would not be rebalanced at all to avoid unnecessarily small trades when there is only a little cash. Defaults for minimum and maximum are 0, resulting in the target range of 0 cash balance.

Minimum (in currency) - define a minimum in the currency for your target range.

Maximum (in currency) - define a maximum in the currency for your target range

- Define how much negative cash balance is increased to cover all negative cash

Define how much negative cash balance is increased when restricting rebalancing to accounts in order to ensure positive cash balance after all trades have gone through, even if the market fluctuates unfavorably. You can define the buffer both as a percentage and in currency when the system would use the value resulting in a larger buffer.

For example, if you have -100€ on your account and the increase is defined as 20% (buffer 100€ * 20% = 20€) and 10€, rebalancing would use cash worth -100€ - 20€ (larger buffer used, 20€ > 10€) = -120€, that is rebalancing would sell more to ensure the negative balance is covered.

Increase as a percentage (%) - define the increase as a percentage.

Increase in currency - define the decrease directly in currency

- Define how much positive cash balance is decreased to ensure a positive cash balance

Define how much positive cash balance is decreased by when restricting rebalancing to accounts in order to ensure a positive cash balance after all trades have gone through, even if the market fluctuates unfavorably. You can define the buffer both as a percentage and in currency when the system would use the value resulting in a larger buffer.

For example, if you have 100€ on your account and the decrease is defined as 20% (buffer 100€ * 20% = 20€) and 10€, rebalancing would use cash worth 100€ - 20€ (larger buffer used, 20€ > 10€) = 80€, that is rebalancing would sell more to ensure the positive balance is covered.

Decrease as a percentage (%) - define the decrease as a percentage.

Decrease in currency - define the decrease directly in currency.

Below, you can define a limit for cash from sales used for buys. This allows you to be more conservative when doing a full rebalance: expected cash from sell orders is used to generate buys within the rebalance in one go but sell order values are not counted as 100% but for example as 90% or 95%. With this, even if prices drop between the time of the rebalance and the time of the execution of your sell orders (and you don't end up getting as much cash from your sales as originally expected), you most likely will get enough cash from your sells to execute your buys (since buys were not generated expecting 100% from your sells but a smaller percentage such as 90% or 95%).

- Define the percent (%) of cash from sales that can be used to buy with

Define a number between 0 and 100. The default is 100, indicating that 100% of cash from sales is used to generate buy orders. This setting is considered when you use a rebalancing method that "buys with cash from sells": this setting limits how big a share of the sell's value is used to generate buy orders.

With this setting, even if prices drop between the time of the rebalance and the time of the sell order execution, you are more to get enough cash from your sells to execute your buys. This is because your buys were not generated expecting 100% from your sells but a smaller percentage such as 90% or 95%.

Example: You have 100€ cash in your account. Position A in your portfolio is 100€ above the target. Position B is 200€ below the target. You are going to do a full rebalance.

If 100% of cash from sells can be used to buy with (default): Considering the available cash in the account and the cash from selling the excess in Position A, the rebalance can buy with: €100 (available cash)+(100%×€100 (from Position A))=€200. Therefore, the rebalance will suggest buying Position B with €200.

If 90% of cash from sales can be used for buys: Considering the available cash in the account and the cash from selling the excess in Position A, the rebalance can buy with €100 (available cash)+(90%×€100 (from Position A))=€190. Therefore, the rebalance will suggest buying Position B with €190.

You can also select what kind of a position listing the summary of the rebalance is shown.

- Aggregate positions in the rebalance window

Allows you to determine how you want the rebalancing window to show your positions, whether you want to aggregate positions or whether you want to group positions per portfolio.

If enabled, positions of all rebalanced portfolios are aggregated (summed up): one row is shown for each position, and the values on the row sum up all positions for that security.

If disabled, positions are grouped by portfolio.

Finally, you can enable rebalancing with real-time 15-minute delayed prices, fetched with a corresponding Market Price Connector from SIX. This allows you to utilize the 15-minute delayed real-time market price feed from SIX to get more up-to-date results from rebalancing your portfolios – the more up-to-date your prices are, the more accurate is the prediction on how much to buy or sell.

- Rebalancing with 15-minute delayed prices

Allows you to rebalance your portfolios with 15-minute delayed real-time prices. Every time you trigger a rebalance on your portfolio(s), the market price connector fetches the latest available prices for all your positions' securities and uses the prices when calculating your trade orders.

Note

Rebalancing will always use the latest available price it can find - if the connector is not enabled, or if you don't get a price through the connector, then the latest available price stored in FA is used. Also, prices fetched from the data connector are converted to portfolio currency with latest FX rates stored in FA when necessary.