Preference - Yield curves

Yield curves are used for valuating contracts and contract-type investments. For details see Steps to set up yield curves for valuating forward cashflows.

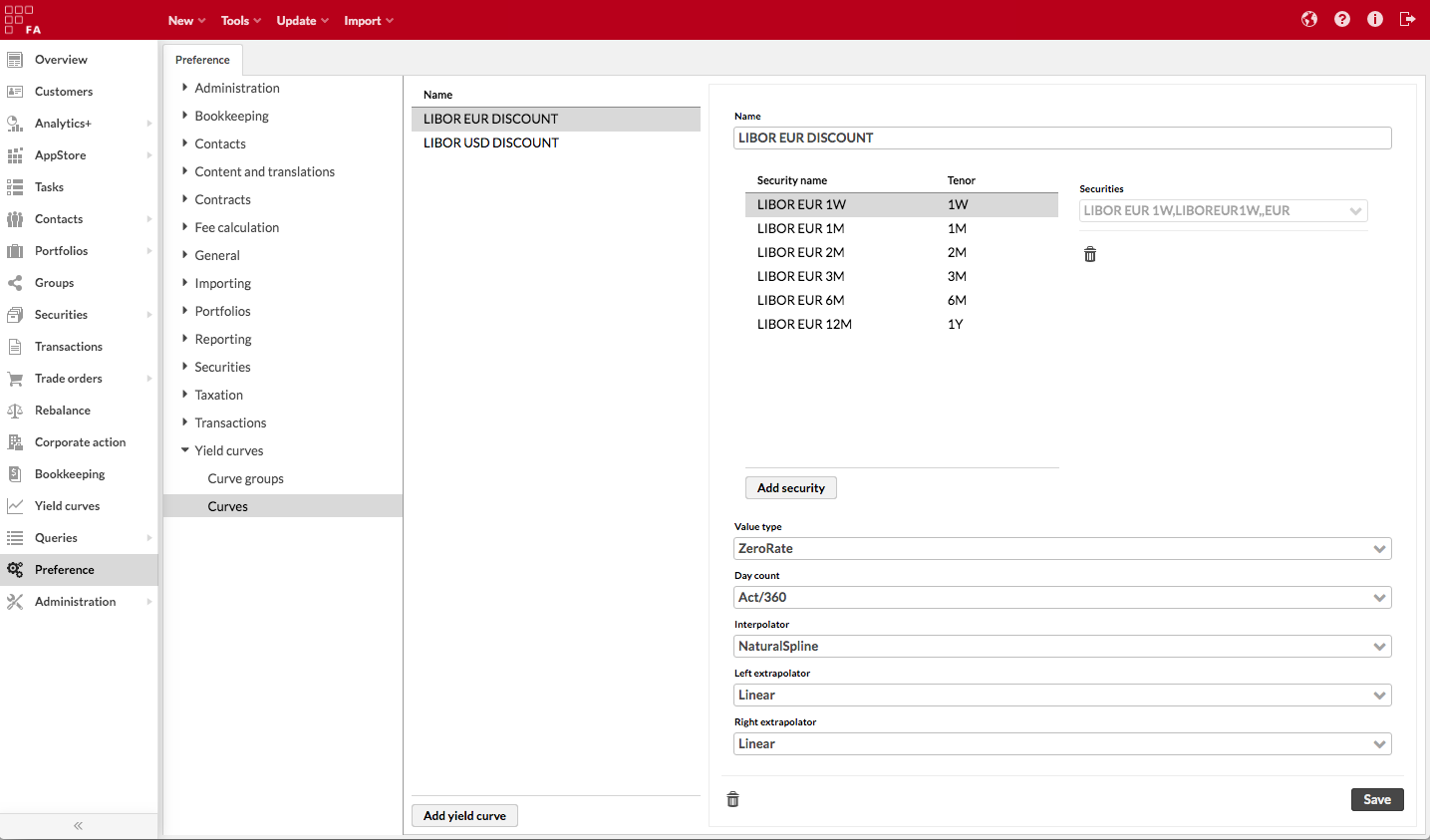

Curves

Yield curve preferences allow you to define individual yield curves in the system. The yield curve is a curve showing several interest rates across different times - yield is known with certainty for a few specific maturity dates, while the other maturities are calculated by interpolation. In FA, the points of the yield curve are defined as securities with different tenors (i.e. time period) and with market data observations containing the valuation information, and the yield curve preferences allow you to form a yield curve from a collection of securities with different tenors.

You can set up a yield curve as a list of securities that together form the yield curve, and give additional settings to describe how values between the observations are interpolated or extrapolated:

- Name

Name of your yield curve, used to identify and select the curve on other preferences and views.

- Securities

Security listing tells you which securities have been linked to the yield curve and with what tenors. The linked security and its tenor tell the yield curve where to fetch the points for each time period when building the curve. You can Add security to add new points to your curve - you need at least two interest-rate securities with different maturities for interpolation to work between them. The linked securities should contain the following relevant configurations:

Tenor - indicate which time period the linked security's values are associated with. You have a variety of options for days (D), weeks (W), months (M), and years (Y) - make sure the tenor corresponds with the values you are getting for the security. You should only add one security with the same tenor to your yield curve.

Market data - Add daily values for your linked securities as market data - These values are used as points of your yield curve. Make sure you get a daily feed for all the linked securities - if an entry is missing from one of the interest rates for one date, the interest rate with that tenor is ignored for that date, and a value is interpolated from other existing interest rates instead.

(Multipliers) - if you are getting the points of your yield curve as percentages from your market data feed (e.g. market date entry 2,73 means interest rate 2,73 %), you should set both multipliers to 100.

- Value type

Select from DiscountFactor or ZeroRate. This setting tells the curve what kind of values you are feeding into the curve, i.e. whether the market data observations on your linked securities are discount factors or rates (e.g. interest rates).

- Day count

Used to determine what kind of calculation value is used to represent one year. Select from available day count conventions.

- Interpolator

Select what kind of an algorithm to use when the system needs to calculate new values between existing values.

- Left extrapolator / Right extrapolator

Select what kind of an algorithm to use when the system needs to calculate new values outside of existing values.

Once a yield curve has been set up, you can see the curve for different valuation dates in the Yield curves view. To show the curve/point of the curve for a certain date, the system fetches the securities linked to the curve, tenor from the security, and market data observations from the security on a given valuation date to show the curve and its values on a certain date.