Valuation of forward cashflows

For valuating forward cashflows, the system calculates the discounted present value of each forward cashflow through relevant yield curves defined in the system. Valuating forward cashflows is a relevant part of managing FX contracts' forward cashflows, but also allows you to manage other forward cashflows, such as Certificates of deposits.

Forward cashflow securities

In order for the system to be able to valuate your forward cashflows, you first need to make sure you have appropriate forward cashflow securities in the system. The forward cashflow securities represents a forward cashflow on a given currency on a given date, and you can reuse the forward cashflow securities on the same currency and date.

For FX Contracts, the appropriate forward cashflow securities are created automatically when saving a contract. If you want to manage other forward cashflows, you can create your forward cashflow securities manually with certain information. Required information to be added for forward cashflow securities for valuation:

Basic info

- Status

Status should be set to Active. Valuation is automatically done only on active securities.

- Type

Type should use the base type DISCOUNT. Valuation is done only on securities with the base type discount.

- Currency

Currency should be set based on the currency of the forward cashflow. Currency is used to find the appropriate discount yield curve from the curve group linking the currency to a curve.

Extra info

- Maturity date

Maturity date should be set as the the maturity date of the forward cashflow. Maturity date is used when calculating the discount factors on the forward cashflow - discount factors are calculated up until the maturity date, and at the maturity date, the discount factor corresponds with the maturity price.

- Maturity price

Maturity price should be set to 1. Maturity price is used when calculating the discount factors on the forward cashflows - on the maturity date, the discount factor corresponds with the maturity price.

Calculating discount factors based on yield curves

Once your forward cashflow securities are in place, the system supports calculating the discounted present value of each forward cashflow through relevant yield curves defined in the system. This is done though calculating discount factors on each forward cashflow security - the sizes of the forward cashflows can vary, but all of them can be valued with the same discount factors.

The discount factors are calculated based on appropriate discount yield curves defined in the system. For more information on setting up yield curves, see Steps to set up yield curves for valuating forward cashflows . Each currency needs a pre-defined discount curve for the system to be able to calculate the discount factors, and the appropriate discount curve is picked based on your forward cashflow security's currency. If a discount curve cannot be found, no discount factors are calculated.

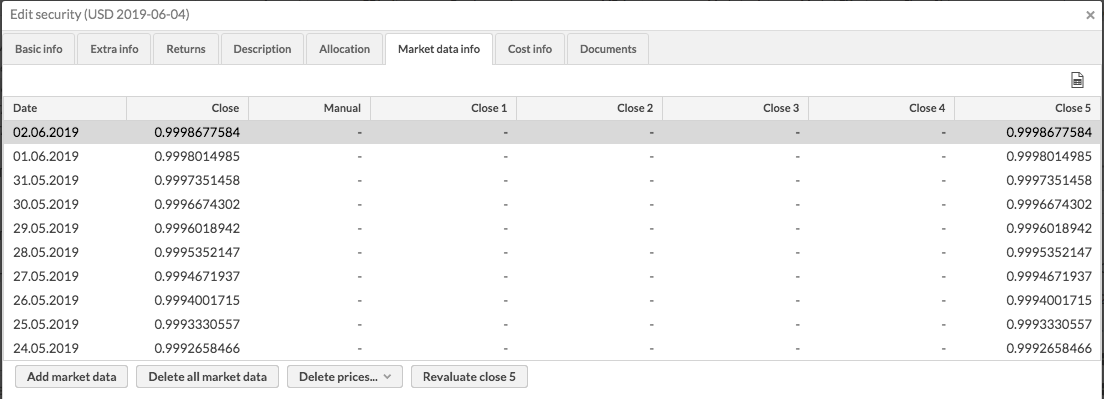

The discount factors are stored under the forward cashflow security's Market data info. Each day's discount factor is stored in the Close 5 field as a market price, indicating how to valuate this forward cashflow on a given date. For each forward cashflow, the system can calculate the discount factors from the beginning of the first position in the security (i.e. when the forward cashflow position is opened with the first transaction) until the maturity date of your forward cashflow security, defined under Extra info. On the maturity date, the discount factor equals to the maturity price defined for your forward cashflow security.

The system uses these discount factors to calculate each day’s market value of your forward cashflow positions. The discount factors can directly be used to valuate the forward cashflow through amount * discount factor = market value.

Automatic and manual valuation

After you have set up your forward cashflow securities correctly and have defined yield curves for all the currencies you want to valuate forward cashflows for, the system provides you with tools for automatic and manual valuation of your forward cashflow securities. Valuation is always done for all appropriate securities regardless of their status.

To keep your forward cashflows up-to-date, the automatic nightly report update valuates all your forward cashflows with new discount factors based on latest yield curve prices. The system automatically valuates your forward cashflows in the following situations:

When saving / modifying a contract that induces forward cashflows. Discount factors are automatically calculated from the beginning of the forward cashflow (i.e. usually from the beginning of the contract) until yesterday (or maturity date, if that is in the past). If the forward cashflow security already exists, only missing discount factors are calculated for the past in case the new contract starts earlier than discount factors currently exist.

During the nightly report data update. Discount factors are automatically calculated daily during the nightly report data update, ensuring you get a new discount factor on your forward cashflows with the latest yield curve prices.

If you are connected to a market data connector to fetch latest end-of-day prices automatically at night, the discount factors are calculated after the new market data observations have been fetched from the connector. Discount factors are calculated for as many days as you get prices for, i.e. as configures in Number of days market prices are fetched for in the nightly run in Market data connector Preferences. Existing discount factors are updated in Close 5 field (other entries not touched).

If you are not connected to a market data connector, the discount factors are calculated as Valuate missing valuations for all securities.

When fetching market data from a market data connector through the Update menu. Discount factors are automatically calculated every time you fetch new market data observations through the menu - this will fetch new prices for you interest rates involved in your yield curves, thus discount factors are recalculated with the new prices. Discount factors are calculated for the same time period you selected to fetch prices for (e.g. 7 days), and Get missing market prices will Valuate missing valuations for all securities. Existing discount factors are updated in Close 5 field (other entries not touched).

In addition, you can manually revaluate your forward cashflow securities through the Security window or Update menu if the appropriate permission to revaluate securities has been enabled for your user role. You can manually valuate your forward cashflows in the following situations:

Revaluate close 5 button in the Security window's Market data info tab is available for securities with base type DISCOUNT and other relevant information. Clicking the button will calculate discount factors

Since the latest existing observation until yesterday or until maturity date, if that is in the past (i.e. since the latest discount factor you can see in the close 5 field until the day you can expect to have close prices for your yield curve interest rates).

If your forward cashflow security doesn't yet have any discount factors, since the beginning of the first position in the security (i.e. when the forward cashflow position is opened with the first transaction) until yesterday or until maturity date, if that is in the past. If you create a forward cashflow security and don't yet have a position on it in a portfolio, discount factors are not calculated.

If you want to revaluate the entire history of your forward cashflow, first Delete Close 5 prices and then Revaluate close 5.

Revaluate all securities menu items in the Update menu allow you to recalculate the discount factors for a specific time period on all your securities with the base type DISCOUNT and other relevant information. Discount factors on a security are never calculated before the beginning of the position or after the maturity date, and all calculations are done until yesterday. Revaluating securities will always trigger a report recalculation to update the effect of the new values to your portfolios - report recalculation will affect all portfolios that contain the securities that receive a new valuation. Options available in the menu are:

Revaluate all securities for past 7 days - recalculates the discount factors for past 7 days, updating the existing discount factors in Close 5 field (other entries not touched).

Revaluate all securities for past 30 days - recalculates the discount factors for past 30 days, updating the existing discount factors in Close 5 field (other entries not touched).

Revaluate all securities for past 365 days - recalculates the discount factors for past 365 days, updating the existing discount factors in Close 5 field (other entries not touched).

Revaluate all securities from [date] - recalculates the discount factors from the shown date (configured Earliest market price date in Market data connector Preferences) onward, updating the existing discount factors in Close 5 field (other entries not touched).

Valuate missing valuations for all securities - recalculates the discount factors since the latest existing observation for each security. This option goes through all relevant securities one-by-one, determines per each security the latest available discount factor, and recalculates discount factors for that security from that date onward. If your forward cashflow security doesn't yet have any discount factors, discount factors are calculated since the beginning of the first position in the security. Depending on the history, your discount might be calculated for different time periods for different securities, depending what their latest available observation is - this option allows you to calculate "valuations that are newer than the newest observation already stored".