Interest rate swaps (IRS)

Interest Rate Swaps can be managed in FA as two opposite Bond transactions. FA does not handle market valuation of Interest Rate Swaps.

Securities

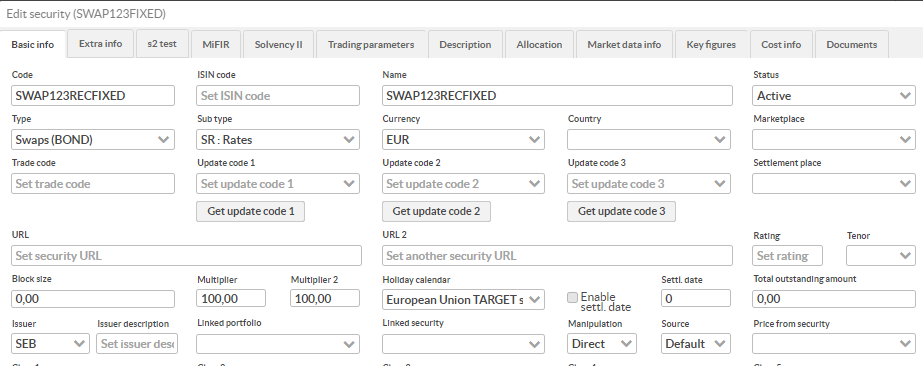

For a swap, two bonds need to be created like in the below example. These securities represent what has the term “legs” using Swap terminology. The bonds is of type Swaps (BOND) and sub type SR : Rates.

It is recommended to use a Security code and name so that fixed and floating leg can be identified belonging to each other. Use a suffix that is logical, indicating both direction (pay or receive), and rate type (fixed or floating). If you have identifiers on legs from external system you may use that on Security code.

The counterparty bank should be set as Issuer, so it is recommended to have the counterparty set up also as contact of type Issuer.

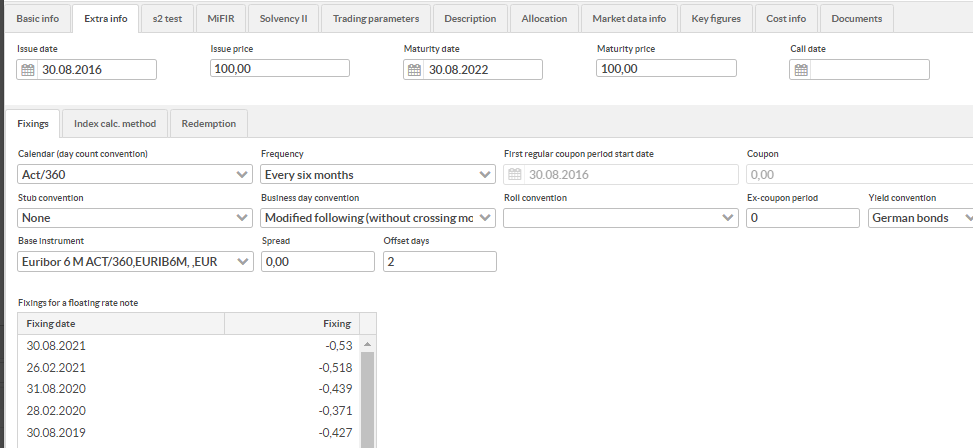

Fixed leg security

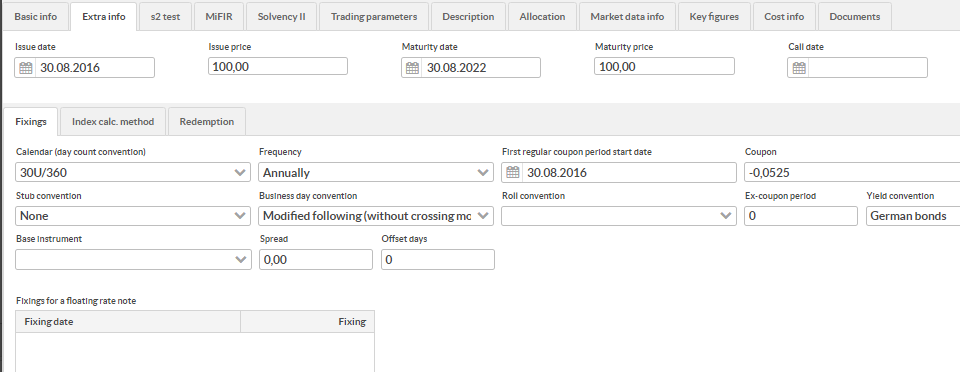

In Extra info tab you enter details of the fixed bond.

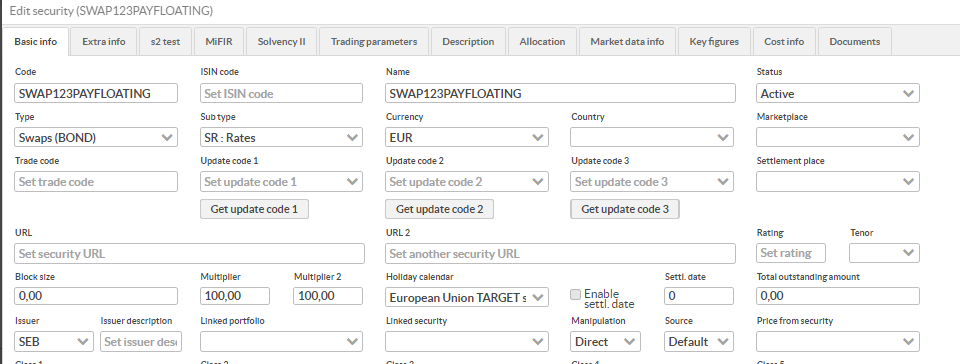

Floating leg security

You need to have the Base instrument defined as Reference instrument (INDEX) of sub-type Interest rate in your system.

Fixings

Given that you have Market data updated on the Base instrument you can set the fixings for Swaps Floating legs in Security view: Update security data - Generate fixings.

Market data info

Prices on Interest Rate Swaps need to be maintained manually or by importing. If prices are received from an external source, these can be imported to FA just by saving a csv file and use Import - Import security prices.

Coupon and maturity processing

Coupon and maturity processing is made with same routines as for Bonds. An important note is that for these Securities it will exist short positions in maturity processing. If a short position transaction type EXPSH - Expire short position must be used instead of EXP - Expire.

Transactions

Transactions in both legs are needed.

Buy us done in the one you RECIEVE the cashflow stream, and sell in the one you pay the cashflow stream (terminology is used even with negative interest rates, when coupon payments are actually opposite).

A good guideline is to save a common identifier for the two legs as Reference. This can be an identifier for the Interest Rate Swap contract in external system. You may also enter Counterparty on transactions.

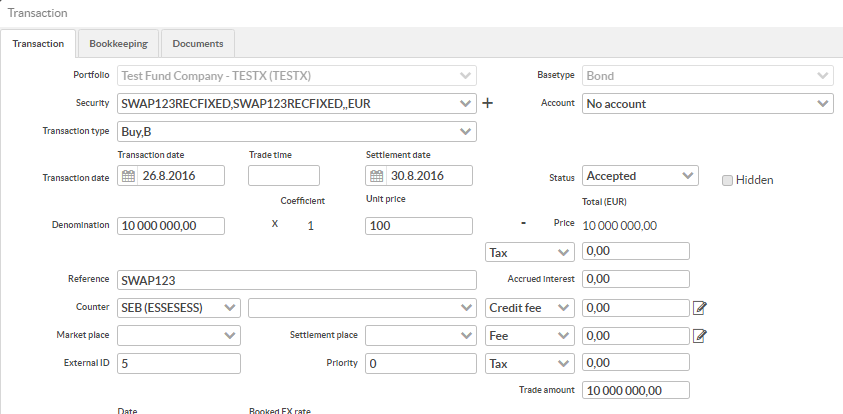

Example buy of fixed rate leg

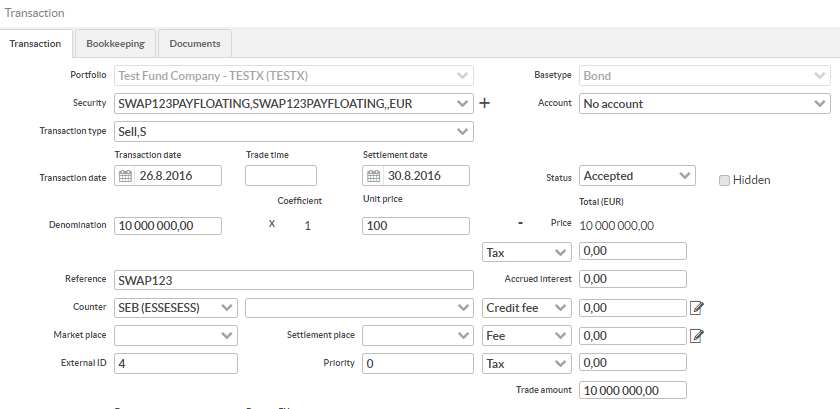

Example sell of floating rate leg

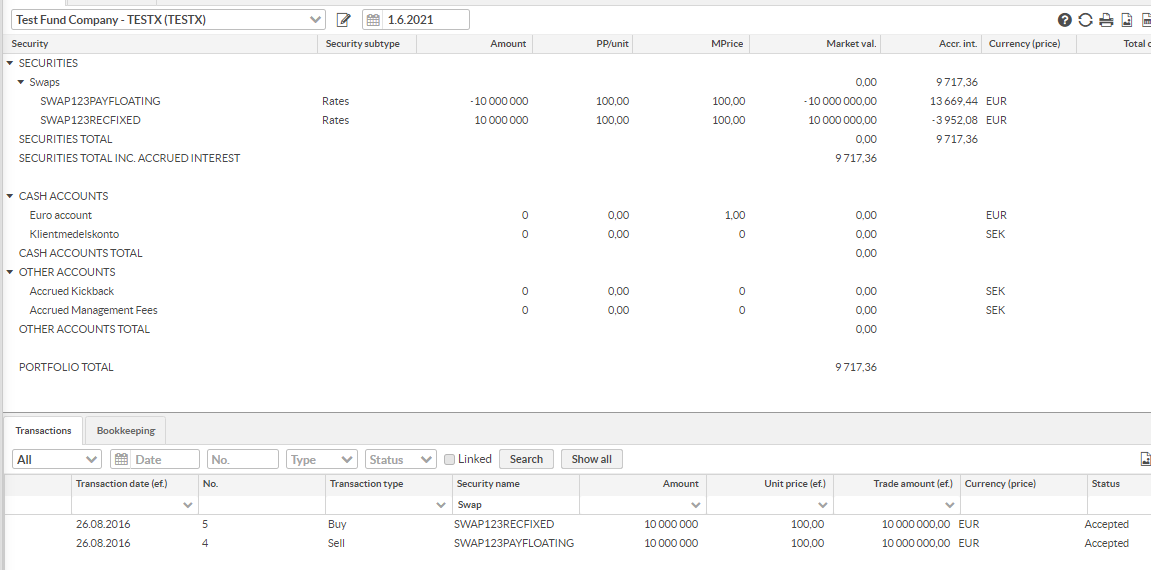

Positions in Interest rate swaps

In Overview and Analytics+, Interest Rate Swaps are shown per leg, as two security positions. See example below from Overview. If differentiating Security name with suffix they will be sorted after each other in these views.