Recording additional assets and liabilities

If your fund has additional valuation factors that you want to consider in the NAV calculation, you can include them in the NAV calculation and record them in a dedicated section of NAV overview. This helps you, for example:

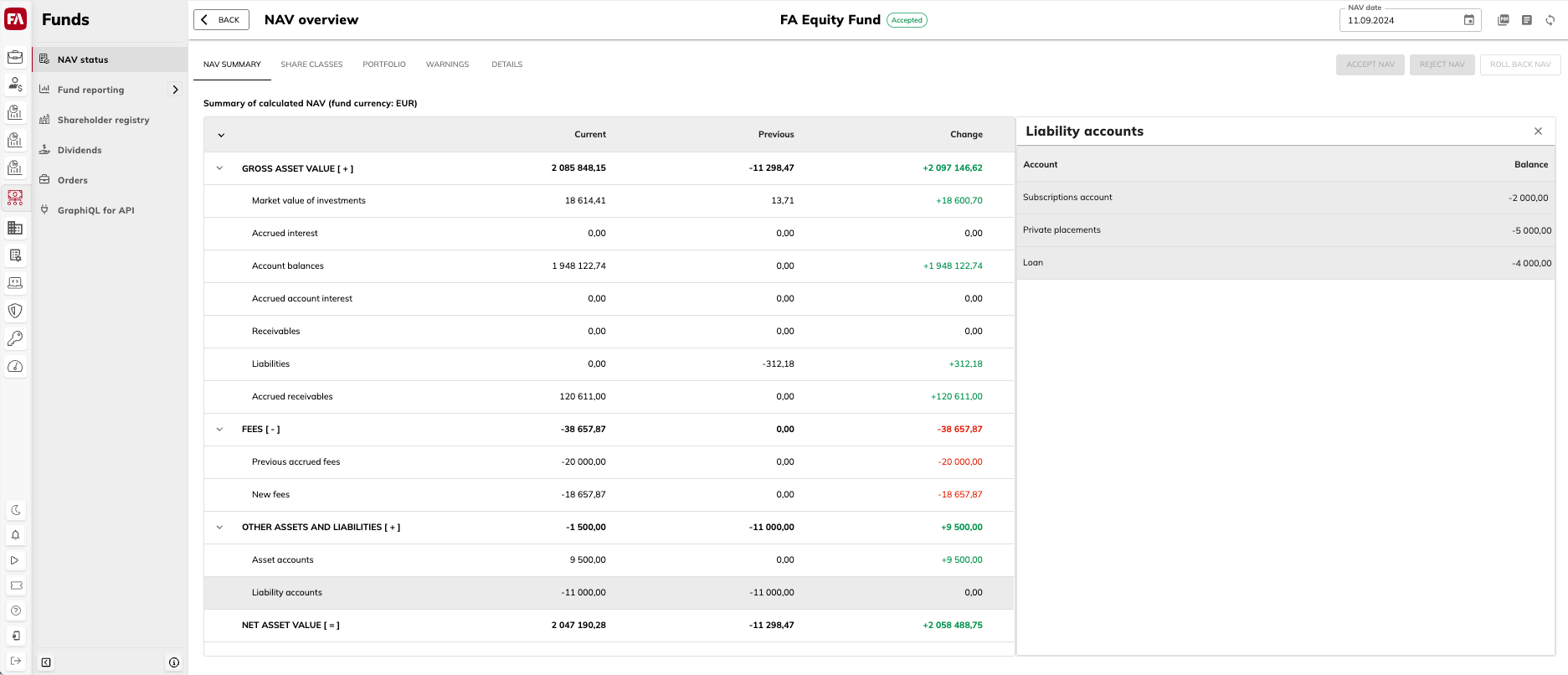

Reflect the private placement restrictions. Since assets acquired through private placements can't be traded for some period, you can record their market value as a liability that reduces NAV. You can also modify the deducted amount iteratively over the period.

Maintain interest-bearing subscription accounts. You can deduct unexecuted subscription amounts from NAV by recording it as a liability. Account interest, on the other hand, will be accrued and included in the GAV calculation.

Offset external loans. You can balance an external loan with a non-cash liability entry to avoid incorrect inflation of NAV with the loan amount.

Handle expected market value rise. You can account for a pending market value rise of a fund's portfolio position by recording it as an asset that increases NAV.

|

Record assets and liabilities in NAV

To record additional assets and liabilities, add them on fund accounts in FA Back:

Create an account for the asset or liability.

Open the fund details panel from the NAV status view in FA Fund management app and click

to open the fund portfolio in FA Back.

to open the fund portfolio in FA Back.Create an account in the Portfolio window, Accounts tab.

Name – Descriptive name that notes the reason for adjustment.

Account type – "Other account".

Other tags – "Exclude from GAV".

Create a transaction that adds or reduces the balance of the account you created.

Transaction type – “Deposit” to add the balance, “Withdrawal” to reduce the balance, or any other type that suits your workflows.

Transaction date – The same as payment date.

Total – The adjustment amount.

Once the fund's NAV is calculated, the account balances are shown in the Other assets and liabilities section in the NAV overview for the fund and in the Share classes tab. Positive balances are summed up in the Asset accounts row. Negative balances are summed up in the Liability accounts row.