Steps to set up yield curves for valuating forward cashflows

In order for the system to be able to valuate the forward cashflow positions generated for your contracts, you need to have appropriate yield curves defined in the system for all currencies involved in your FX contracts. These discount curves are used to calculate the discount factors for each forward cashflow security until maturity, and the discount factors are then used to calculate the net present value of your forward cashflow on any historical date.

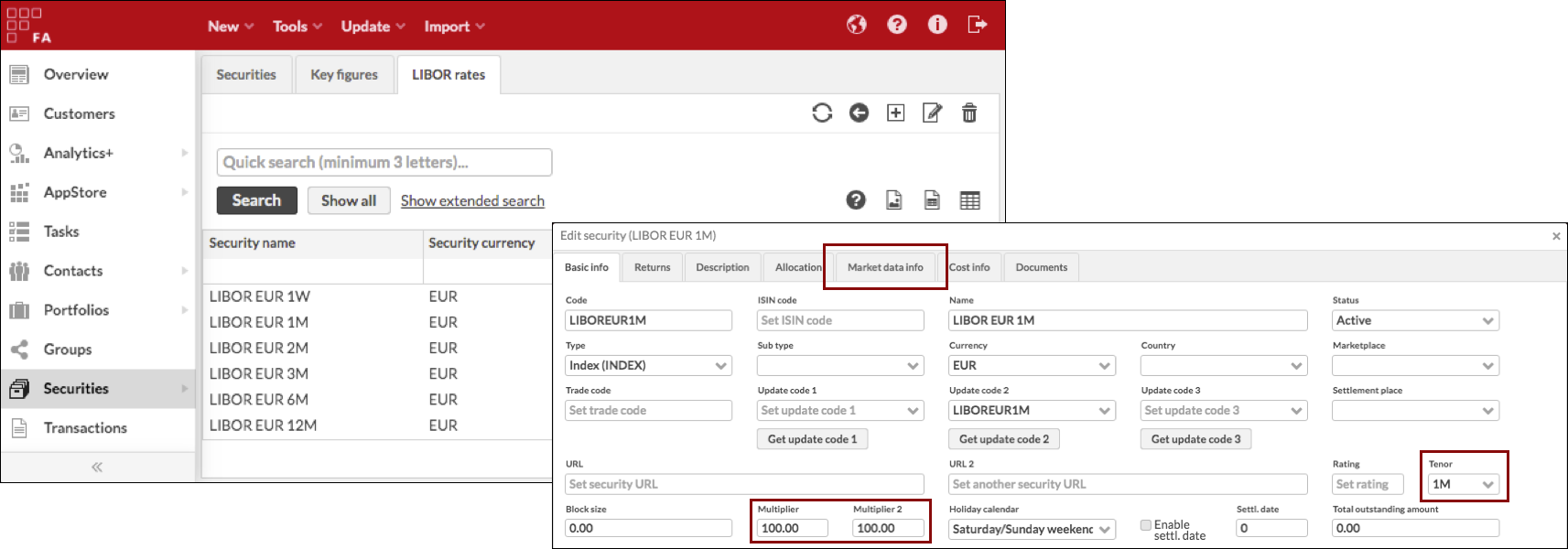

Step 1 - Create securities for the interest rates you want to use as points in your yield curve

First step is to set up the interest rates you want to use as points in your yield curve. You need at least two interest rates with different maturities for interpolation to work between them - however, you can add as many interest rates you'd like to use to build your curve. For example, you can set up interest rates for LIBOR EUR 1W, 1M, 2M, 3M, 6M and 12M.

You can set up your interest rates as securities in the system (i.e. one security for each interest rate with different maturity). Set descriptive codes and names and an appropriate currency to the interest rate securities, and pay close attention to the following relevant configurations:

- Tenor

Indicate which tenor the interest rate is associated with, i.e. the duration / maturity of the interest rate. You have a variety of options for days (D), weeks (W), months (M) and years (Y) - make sure the tenor corresponds with the interest rate you are defining. For example, for the rate "LIBOR EUR 1W" select tenor "1W" and for "LIBOR EUR 12M" select tenor "12M".

- Multipliers

Often you receive the market data for your interest rates as "percentage rates" (i.e. market date entry 2,73 means interest rate 2,73 %). In order for all calculations to work with percentage values, set both Multiplier and Multiplier 2 to 100.

- Market data

If you set both multipliers to 100, make sure your interest rates feed in as percentages. For valuation to work, make sure you get a daily interest rate feed for all the interest rates you have defined in the system and are planning to use in your yield curve - if an entry is missing from one of the interest rates for one date, the interest rate with that tenor is ignored for that date, and a value is interpolated from other existing interest rates instead.

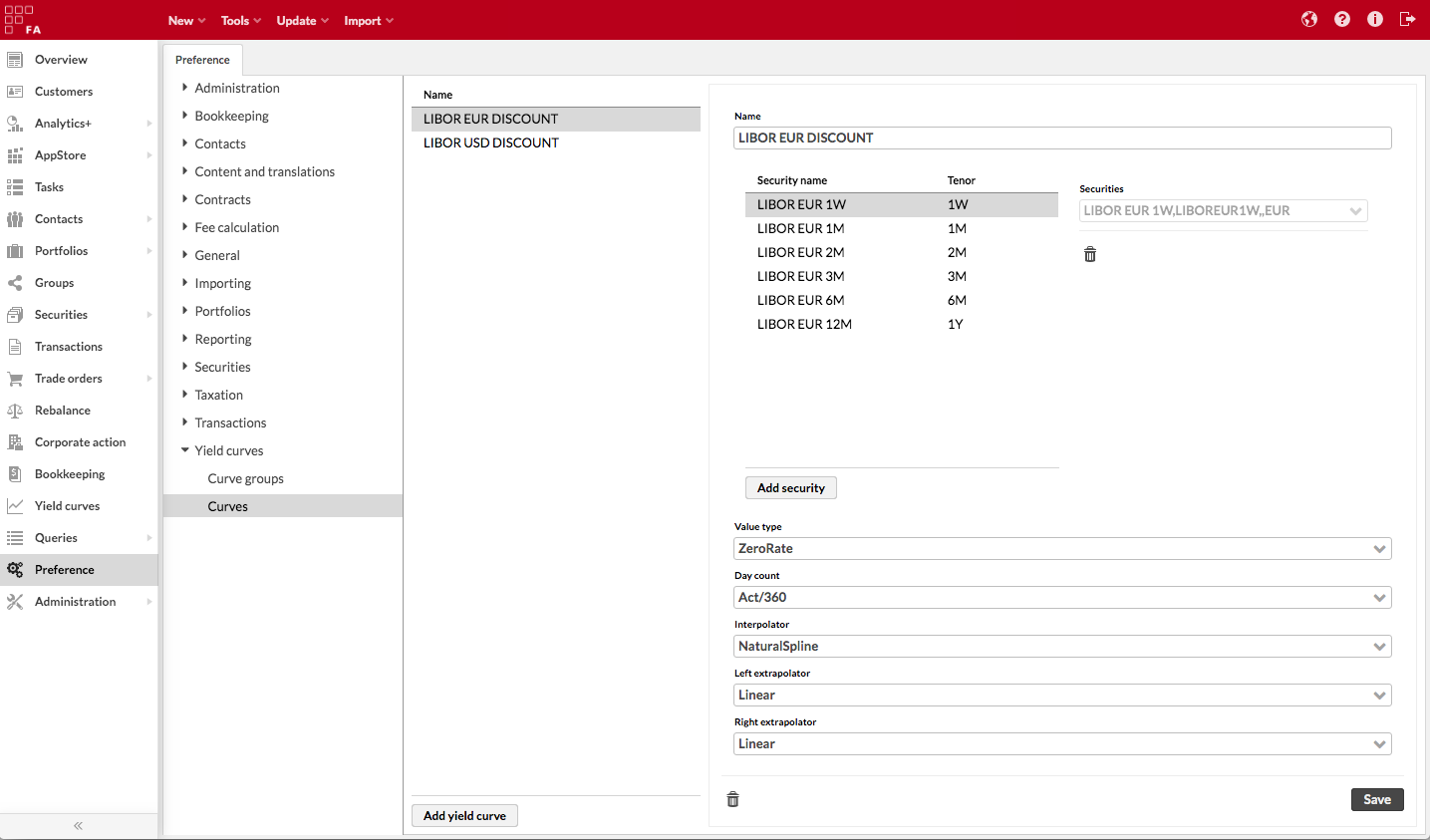

Step 2 - Create a discount curve for each currency you want to valuate forward cashflows with

Second step is to set up yield curves out of the interest rates you defined in step 1. You should set up a yield curve for each currency involved in you FX contracts - if you want to valuate forward cashflows for the currency, you need to have a discount yield curve in place for the currency. For example, you can set up yield curves for LIBOR EUR DISCOUNT and LIBOR USD DISCOUNT.

You can set up your yield curves under the Yield curves preferences (i.e. one curve for each currency). Set descriptive names to the curves, and pay close attention to the following relevant configurations:

- Security

Add the interest rates you defined in step 1 as securities - the security and its tenor tells the yield curve where to fetch the points for each day when building the curve. The securities you link should have the appropriate tenor, and you should only add one security with the same tenor. You need at least two interest rate securities with different maturities for interpolation to work between them.

- Value type

Select ZeroRate as the value type if your interest rate securities get their market data as interest rates.

In addition, select an appropriate day count for your curve, and select appropriate interpolators / extrapolators.

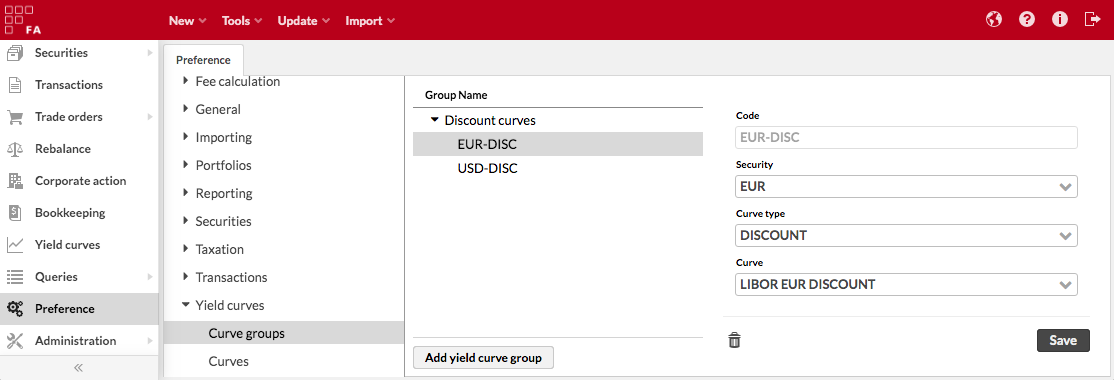

Step 3 - Create a curve group for your currency discount curves

Third step is to create curve groups out of the yield curves you defined in step 2. Curve groups allow you to indicate which curve should be used for which currency, and that the yield curve you defined should be used as a discount curve. For example, you can link your LIBOR EUR DISCOUNT curve to your EUR currency as a DISCOUNT curve, when the system knows to use LIBOR EUR DISCOUNT curve to discount forward cashflows in EUR.

You can set up your yield curve groups under the Yield curves preferences. First, Add a yield curve group for "Discount curves", and under the group, Add group item for each currency + discount curve pair. The code is automatically generated based on your selections:

- Security

Select the currency you want to link a discount curve to.

- Curve type

Select curve type DISCOUNT.

- Curve

Select the curve you created in step 2.

After this, the forward cashflows in the currency are discounted with the linked curve.